For CFOs and finance leaders, cash flow visibility plays a direct role in liquidity management, risk oversight, and day-to-day operational decisions.

Traditional cash flow statements often explain what happened. The challenge today is understanding what is happening now and what is likely to happen next.

A Cash Flow Management Dashboard in Power BI, aligned with IAS 7 (Statement of Cash Flows), offers a dynamic, data-driven solution for tracking and analyzing an entity’s cash flows. This dashboard enables businesses to visualize and manage cash inflows, outflows, and liquidity across various activities (operating, investing, and financing). By integrating IAS 7 standards, the dashboard ensures that cash flow data is presented in a standardized format, making it easier to assess the financial health of an organization. With real-time insights, decision-makers can evaluate the timing, amount, and certainty of future cash flows, optimize liquidity, and improve forecasting, all within an intuitive Power BI interface. This dashboard empowers businesses to make informed, strategic financial decisions while ensuring compliance with international accounting standards.

Our Data-Driven Cash Flow Monitoring Dashboard Using Power BI and IAS7 has been designed to answer questions such as:

- Key Definitions

- Scope of the Cash Flow Statement

- Components of Cash and Cash Equivalents

- How CFOs Monitor Cash Flow Effectively Under IAS 7

- Key Principles of Effective Cash Flow Management

- How do you manage cash flow effectively?

- The Three-Step Framework for Cash Flow Control

- Non-cash transactions

- Why the Cash Flow Statement Matters for Liquidity and Risk Management

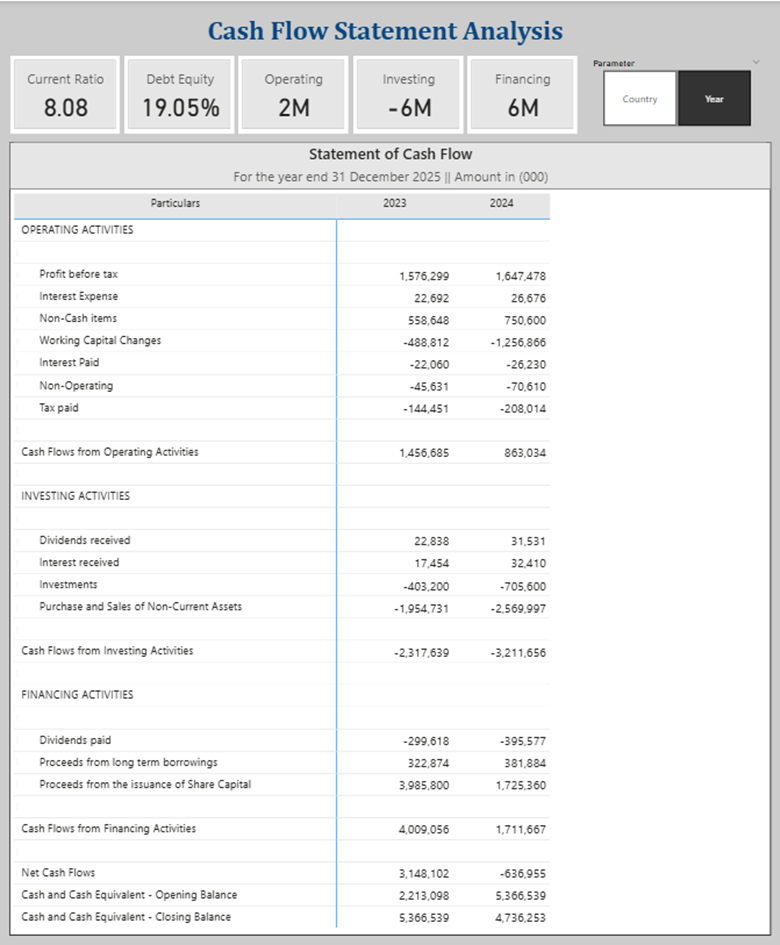

This report offers both value by Country and Year, allowing users to seamlessly switch between them with a single click for improved as required.

Key Definitions:

These definitions form the foundation of IAS 7 and are critical for interpreting cash flow data correctly, especially when dashboards are used for executive decision-making.

- Cash flow Cash equivalents are short‑ term, highly liquid investments that are readily convertible to known amounts of cash and which are subject to an insignificant risk of changes in value. Cash flows are inflows and outflows of cash and cash equivalents.

- Operating activities are the principal revenue‑ producing activities of the entity and other activities that are not investing or financing activities.

- Investing activities are the acquisition and disposal of long‑ term assets and other investments not included in cash equivalents.

- Financing activities are activities that result in changes in the size and composition of the contributed equity and borrowings of the entity.

Scope of the Cash Flow Statemetn:

An entity shall prepare a statement of cash flows in accordance with the requirements of the IAS-7 and shall present it as an integral part of its financial statements for each period for which financial statements are presented.

Focus on cash and cash equivalents: The statement in intended to show how the entity generates and uses cash and cash equivalents.

Why it matters: Users need this information because entities require cash to:

- Run operation

- Settle obligations, and

- Provide returns to investors.

Components of Cash and Cash Equivalents

Under IAS 7, the components of cash and cash equivalents must be clearly defined to ensure transparency. These assets are considered highly liquid and can be easily converted into cash within a short period.

Key Components Include:

- Cash on hand: Physical cash available for immediate use.

- Demand deposits: Balances in bank accounts that can be withdrawn on demand.

- Short-term, highly liquid investments: Investments like treasury bills, certificates of deposit, and money market instruments with maturities of three months or less.

- Marketable securities: Assets that can be quickly liquidated with minimal loss.

How CFOs Monitor Cash Flow Effectively Under IAS 7

Effective cash flow monitoring involves continuously assessing an entity’s inflows and outflows to ensure sufficient liquidity to meet obligations and support growth. This process is aligned with IAS 7 – Statement of Cash Flows, which requires businesses to categorize cash flows into operating, investing, and financing activities to assess an entity’s capacity to generate cash.

Steps to Monitor Cash Flow:

- Tracking inflows and outflows: Recognize and document all incoming and outgoing cash, including operational revenue, loan receipts, and capital expenditures.

- Use of forecasting: A robust forecast is essential for predicting cash needs and avoiding liquidity issues, as emphasized in the Conceptual Framework for Financial Reporting [paragraphs 4.30–4.35] which highlights the importance of providing information for users to assess future cash flows.

- Regular reporting: Financial statements must provide accurate cash flow data in line with IAS 7 to ensure stakeholders can assess the firm’s financial position and liquidity.

Key Principles of Effective Cash Flow Management

Managing cash flow effectively requires maintaining an optimal balance between cash inflows and outflows, ensuring that an organization can continue operations without financial strain. According to IAS 7, this balance is essential for sustainable growth.

Key Aspects of Cash Flow Management:

- Speed of Receivables: Efficient management of receivables helps shorten the cash conversion cycle. IAS 7 emphasizes the importance of converting operating activities into cash to support daily operations.

- Optimizing Payables (without impacting relationships): Extending payment terms to suppliers helps businesses hold onto cash for longer periods.

- Cash Flow Forecasting: IAS 7 suggests that organizations should develop cash flow forecasts to plan for potential deficits, ensuring sufficient liquidity to meet obligations.

How do you manage cash flow effectively?

To manage cash flow effectively, businesses must implement a combination of strategic planning and daily oversight. The IFRS Framework emphasizes the importance of providing information about an entity’s liquidity and solvency, which directly correlates with cash flow management.

Practical Strategies for Effective Management:

- Monitor Cash Flow Trends: Regular analysis of cash flow data and trends aids in making adjustments to operations and finance strategies, ensuring there are no surprises at the end of the month.

- Optimize Working Capital: Managing inventory, receivables, and payables efficiently is a key factor in maintaining cash flow, as IAS 7 advises entities to evaluate cash movements in operational terms.

- Ensure Adequate Liquidity: Companies should hold sufficient cash reserves for operational needs and unexpected financial obligations, in line with IAS 7‘s requirement to disclose cash equivalents in the financial statements.

- Develop Financial Models: Cash flow forecasting models based on past data and external factors help predict future financial needs.

The Three-Step Framework for Cash Flow Control

Following a structured approach is key to managing cash flow effectively. According to IAS 7, businesses should focus on three main areas of cash flow:

- Monitor Cash Inflows: Cash inflows include revenue from sales, capital contributions, and loan receipts. By tracking these, businesses can assess their revenue-generating abilities and decide when additional financing might be necessary.

- Monitor Cash Outflows: This includes all cash outflows such as payments to suppliers, employees, and creditors. Businesses must track these to ensure that they don’t exceed the available inflows and lead to liquidity issues.

- Forecast Future Cash Flows: Cash flow forecasting is critical for ensuring adequate liquidity for operations and investments. IAS 7 recommends that entities use historical data to forecast future cash needs, which helps to ensure financial stability.

- Non-Cash Transactions

Non-cash transactions, as defined in IAS 7, are those that impact an entity’s financial position but do not involve the movement of cash. These are critical to understand because they affect the balance sheet and financial statement presentation.

Examples of Non-Cash Transactions:

- Depreciation and Amortization: Non-cash expenses that reflect the reduction in value of assets but do not affect cash.

- Issuance of Shares: Issuing stock in exchange for assets, which affects the equity portion of the balance sheet but does not involve cash.

- Debt Forgiveness: When creditors forgive outstanding debts, this affects liabilities without a direct cash outflow.

- Why the Cash Flow Statement Matters for Liquidity and Risk Management

The cash flow statement is one of the key financial statements and provides essential information about an entity’s cash inflows and outflows. According to IAS 7, this statement is integral for evaluating the liquidity, solvency, and financial flexibility of a business.

Key Benefits:

- Improved liquidity management: The cash flow statement helps assess the entity’s ability to generate sufficient cash to meet operational and financial needs, which is critical for maintaining liquidity.

- Enhanced decision-making: By providing clear visibility into cash movements, it allows management to make better strategic decisions regarding investments, financing, and operations.

- Accurate financial health assessment: Investors, creditors, and other stakeholders rely on the cash flow statement to assess the long-term viability and risk of a company, aligning with the IFRS Conceptual Framework which emphasizes transparency in financial reporting.

- Facilitates comparisons: Standardized reporting of cash flows under IAS 7 allows businesses to be compared against industry peers and competitors on a like-for-like basis.

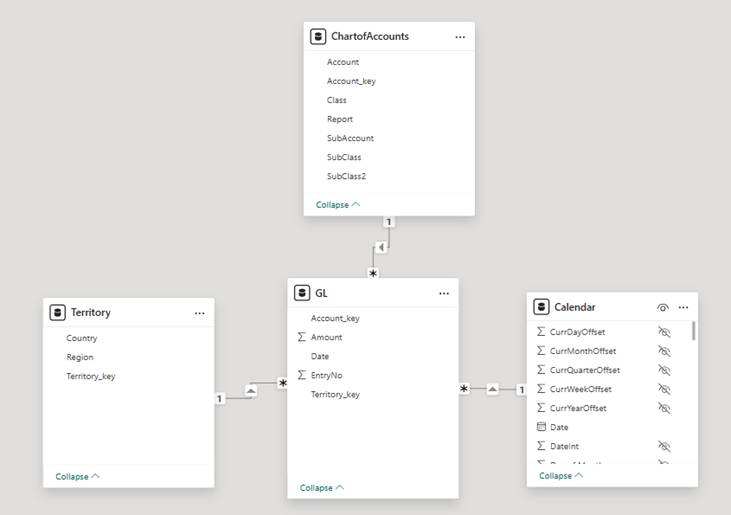

Data Model Overview for Cash Flow Management

We can see the data model used for building the Cash Flow Management Dashboard in Power BI. The relationships between tables like Chart of Accounts, GL (General Ledger), Territory, and Calendar are crucial for enabling efficient and accurate analysis of cash flow data.

- Chart of Accounts: This table provides the structure of the accounts, with detailed classifications such as Account, Class, and SubAccount. This allows for a clear understanding of how each account is grouped and classified.

- GL: The General Ledger (GL) is at the heart of the financial transactions, capturing amounts, account keys, and dates for each transaction entry.

- Territory: Territory information allows for geospatial analysis of financial data, helping identify cash flows by region or country.

- Calendar: This table enables time-based analysis by connecting transactions to specific time periods (e.g., month, quarter, year), ensuring cash flow data can be segmented appropriately.

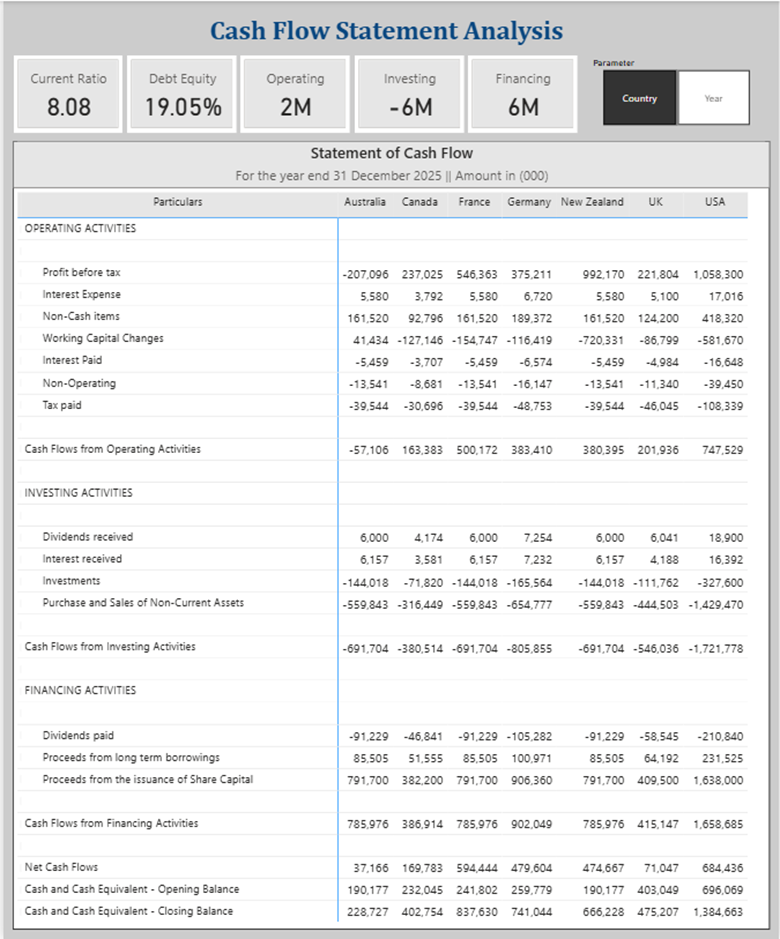

Cash Flow Statement Analysis:

Cash Flow Statement Dashboard Insights:

- Operating Activities (863K) – The majority of cash flow comes from operations, indicating that the core business is generating positive cash flow.

- Investing Activities (-3M) – Negative cash flow, as expected in investing activities, primarily due to purchases of non-current assets.

- Financing Activities (2M) – Positive cash flow due to proceeds from share capital issuance, showcasing a healthy financing structure and investor confidence.

- Cancelled Orders (4.38%) – While a smaller portion of the business, monitoring cancelled orders provides critical insights into potential operational inefficiencies like stockouts or delayed shipments.

Decision Support:

- Healthy Operating Cash Flow: Highlights the company’s ability to fund operations from its core activities, helping ensure liquidity for short-term and long-term financial needs.

- Investing Focus: Negative cash flow in investing activities suggests capital allocation towards asset acquisition; valuable for strategic growth but requires careful monitoring of cash reserves.

- Financing Health: Positive financing cash flow indicates strong support from investors and capital markets, strengthening the business’s ability to meet future obligations.

- Order Fulfillment Focus: The attention to cancelled orders helps uncover operational bottlenecks and improves customer satisfaction by addressing the root causes of cancellations.

Card Visual for Key Insights

- Current Ratio (8.08): Indicates strong liquidity, with sufficient assets to cover short-term liabilities.

- Debt to Equity (19.05%): Shows low debt compared to equity, indicating conservative leverage.

- Operating Cash Flow (2M): Positive cash flow from core operations.

- Investing Cash Flow (-6M): Negative cash flow, indicating investment spending.

- Financing Cash Flow (6M): Positive cash flow, suggesting inflows from financing activities.

Fields Parameter

The parameter slicer allows users to dynamically switch between Country and Year in the report. This enables flexible data analysis, where selecting Year or Country updates the visuals accordingly, providing a tailored view of the data based on user preference

Conclusion

In practice, a Cash Flow Management Dashboard built in Power BI and aligned with IAS 7 moves cash flow analysis beyond static reporting. Instead of looking at cash movements after the fact, finance teams gain continuous visibility into operating, investing, and financing activities as they evolve over time.

For CFOs and finance leaders, this translates into stronger control over liquidity, earlier identification of potential risks, and more reliable input for forecasting and capital allocation decisions. When cash inflows and outflows are structured consistently and updated in near real time, discussions shift from reconciling numbers to understanding implications and planning next steps.

When cash flow data is timely, transparent, and trusted, finance leaders can spend less time validating reports and more time steering the business with confidence.

Report: Cash Flow Management